All Categories

Featured

Table of Contents

For earning a limited amount of the index's growth, the IUL will never receive much less than 0 percent passion. Even if the S&P 500 declines 20 percent from one year to the following, your IUL will certainly not lose any kind of cash money value as an outcome of the marketplace's losses.

Imagine the interest compounding on a product with that kind of power. Offered all of this information, isn't it possible that indexed universal life is an item that would enable Americans to acquire term and spend the rest?

A real investment is a safeties item that goes through market losses. You are never subject to market losses with IUL simply because you are never subject to market gains either. With IUL, you are not purchased the marketplace, yet just making interest based upon the efficiency of the market.

Returns can grow as long as you continue to make settlements or keep an equilibrium.

No Lapse Universal Life Insurance

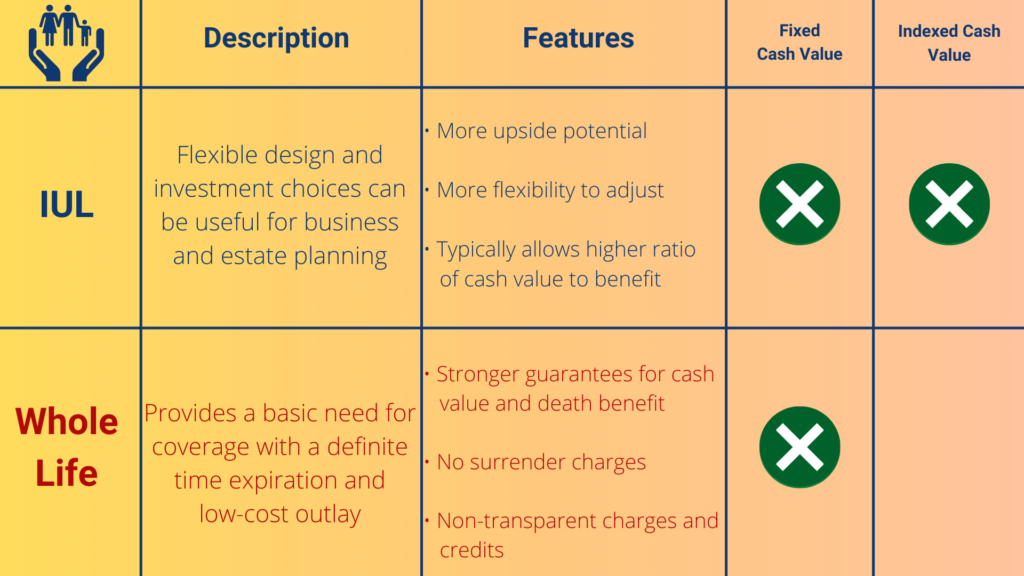

Unlike universal life insurance policy, indexed universal life insurance policy's cash money worth earns rate of interest based on the performance of indexed securities market and bonds, such as S&P and Nasdaq. It isn't directly invested in the stock market. Mark Williams, Chief Executive Officer of Brokers International, states an indexed global life policy is like an indexed annuity that feels like global life.

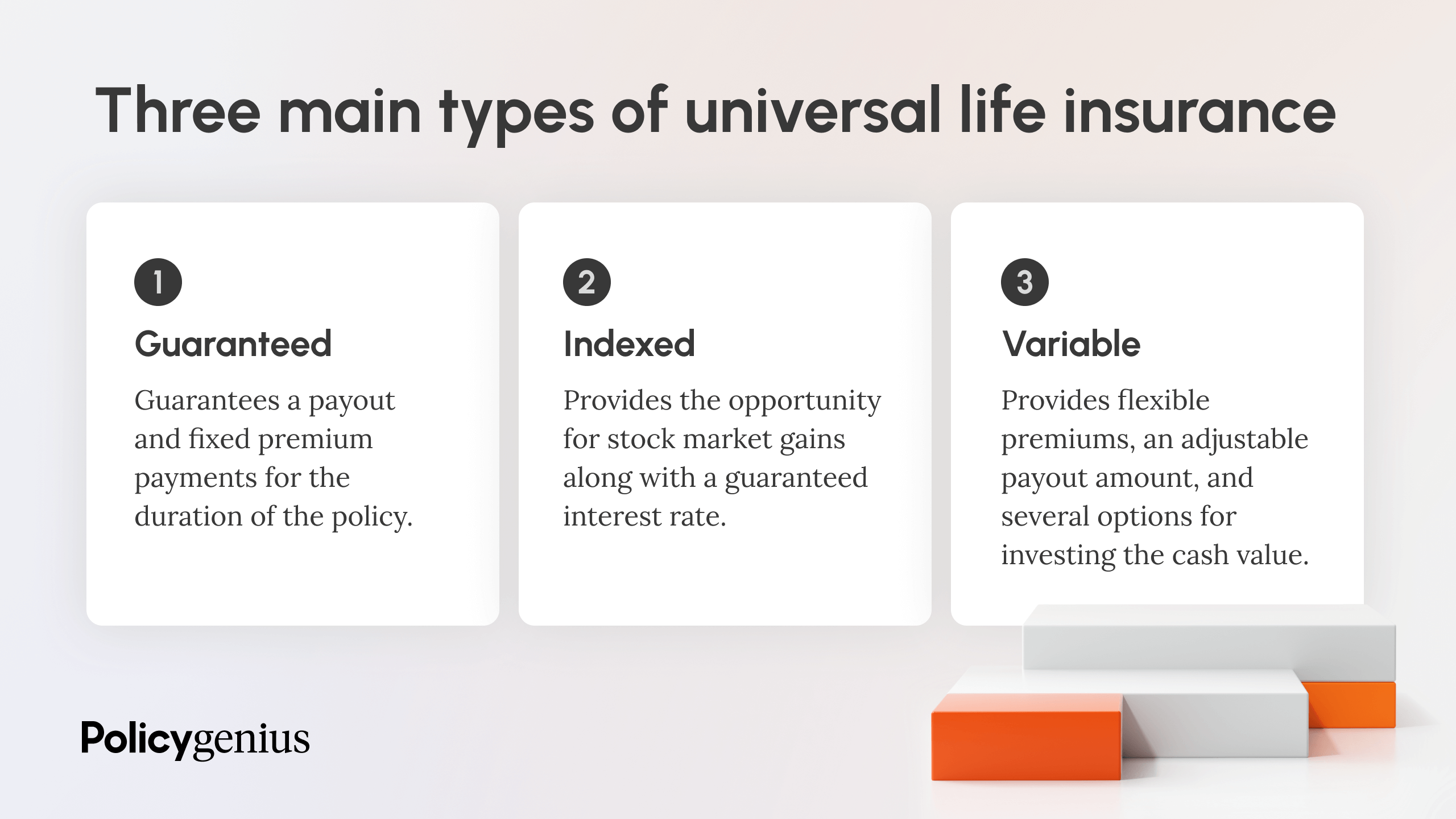

Universal life insurance policy was produced in the 1980s when interest prices were high. Like various other types of long-term life insurance, this policy has a cash money value.

Indexed global life policies use a minimum guaranteed rate of interest price, also understood as an interest crediting floor, which lessens market losses. Claim your cash value loses 8%.

Best Universal Life Insurance

It's additionally best for those going to assume extra danger for greater returns. A IUL is an irreversible life insurance policy policy that borrows from the residential or commercial properties of a global life insurance policy. Like global life, it enables adaptability in your survivor benefit and premium repayments. Unlike universal life, your money value grows based upon the performance of market indexes such as the S&P 500 or Nasdaq.

Her job has been published in AARP, CNN Highlighted, Forbes, Fortune, PolicyGenius, and United State News & Globe Report. ExperienceAlani has reviewed life insurance policy and pet dog insurer and has created various explainers on travel insurance, credit scores, financial debt, and home insurance policy. She is passionate about demystifying the complexities of insurance policy and various other individual financing subjects to make sure that readers have the information they need to make the very best money decisions.

Paying only the Age 90 No-Lapse Premiums will guarantee the death advantage to the insured's acquired age 90 however will certainly not guarantee cash value buildup. If your client stops paying the no-lapse assurance costs, the no-lapse attribute will end prior to the ensured period. If this occurs, added costs in an amount equal to the shortage can be paid to bring the no-lapse feature back in pressure.

I lately had a life insurance policy sales person show up in the remarks string of a blog post I published years ago regarding not blending insurance coverage and investing. He thought Indexed Universal Life Insurance Coverage (IUL) was the most effective point since cut bread. On behalf of his setting, he published a link to an article composed in 2012 by Insurance Agent Allen Koreis in 2012, qualified "16 Reasons Accountants Prefer Indexed Universal Life Insurance Policy" [link no longer offered]

Iul Life Insurance Meaning

Initially a quick explanation of Indexed Universal Life Insurance. The attraction of IUL is noticeable.

If the marketplace goes down, you obtain the assured return, generally something in between 0 and 3%. Naturally, because it's an insurance coverage policy, there are likewise the usual costs of insurance policy, compensations, and abandonment fees to pay. The information, and the factors that returns are so awful when blending insurance policy and investing in this specific method, come down to primarily three things: They just pay you for the return of the index, and not the returns.

Adjustable Premium Life Insurance

If you cap is 10%, and the return of the S&P 500 index fund is 30% (like last year), you obtain 10%, not 30%. If the Index Fund goes up 12%, and 2% of that is dividends, the change in the index is 10%.

Add all these results with each other, and you'll discover that lasting returns on index global life are pretty darn near to those for whole life insurance policy, favorable, however low. Yes, these plans assure that the cash money worth (not the cash that mosts likely to the prices of insurance, naturally) will not lose money, however there is no guarantee it will stay on top of inflation, much less grow at the price you require it to grow at in order to attend to your retirement.

Koreis's 16 factors: An indexed universal life plan account value can never ever lose cash as a result of a down market. Indexed global life insurance policy warranties your account worth, securing gains from each year, called an annual reset. That holds true, however only in nominal returns. Ask on your own what you need to pay in order to have a guarantee of no small losses.

In investing, you make money to take danger. If you don't want to take much risk, do not anticipate high returns. IUL account worths grow tax-deferred like a qualified strategy (IRA and 401(k)); common funds do not unless they are held within a certified plan. Put simply, this implies that your account value gain from three-way compounding: You make rate of interest on your principal, you gain interest on your rate of interest and you make passion accurate you would certainly or else have paid in taxes on the rate of interest.

Universal Life Insurance Reviews

Although qualified strategies are a far better option than non-qualified strategies, they still have issues not offer with an IUL. Financial investment options are usually limited to mutual funds where your account value goes through wild volatility from direct exposure to market threat. There is a big difference between a tax-deferred pension and an IUL, however Mr.

You buy one with pre-tax bucks, conserving on this year's tax obligation expense at your low tax price (and will usually have the ability to withdraw your cash at a reduced effective rate later) while you spend in the other with after-tax dollars and will be required to pay passion to borrow your very own cash if you don't want to surrender the plan.

He tosses in the timeless IUL salesman scare tactic of "wild volatility." If you despise volatility, there are much better means to decrease it than by acquiring an IUL, like diversification, bonds or low-beta supplies. There are no constraints on the quantity that may be added yearly to an IUL.

:max_bytes(150000):strip_icc()/dotdash-comparing-iul-insurance-iras-and-401ks-Final-71f14693e37d4fb1b0736112179802b5.jpg)

That's guaranteeing. Allow's consider this for a 2nd. Why would certainly the government placed limits on how much you can take into retired life accounts? Perhaps, just maybe, it's since they're such a large amount that the federal government doesn't want you to conserve way too much on taxes. Nah, that couldn't be it.

{kind=link}

Table of Contents

Latest Posts

Eiul Life Insurance

Aig Index Universal Life Insurance

Universal Term Life

More

Latest Posts

Eiul Life Insurance

Aig Index Universal Life Insurance

Universal Term Life